Europe likes the word sovereignty. It has a good mouthfeel: stern, historical, expensive enough to sound serious.

So now we have digital sovereignty, technological sovereignty, and AI sovereignty. These phrases arrive accompanied by funds, summits, frameworks, and a mild smell of institutional perfume. One could almost believe that sovereignty is achieved by naming it in a room full of laminated badges.

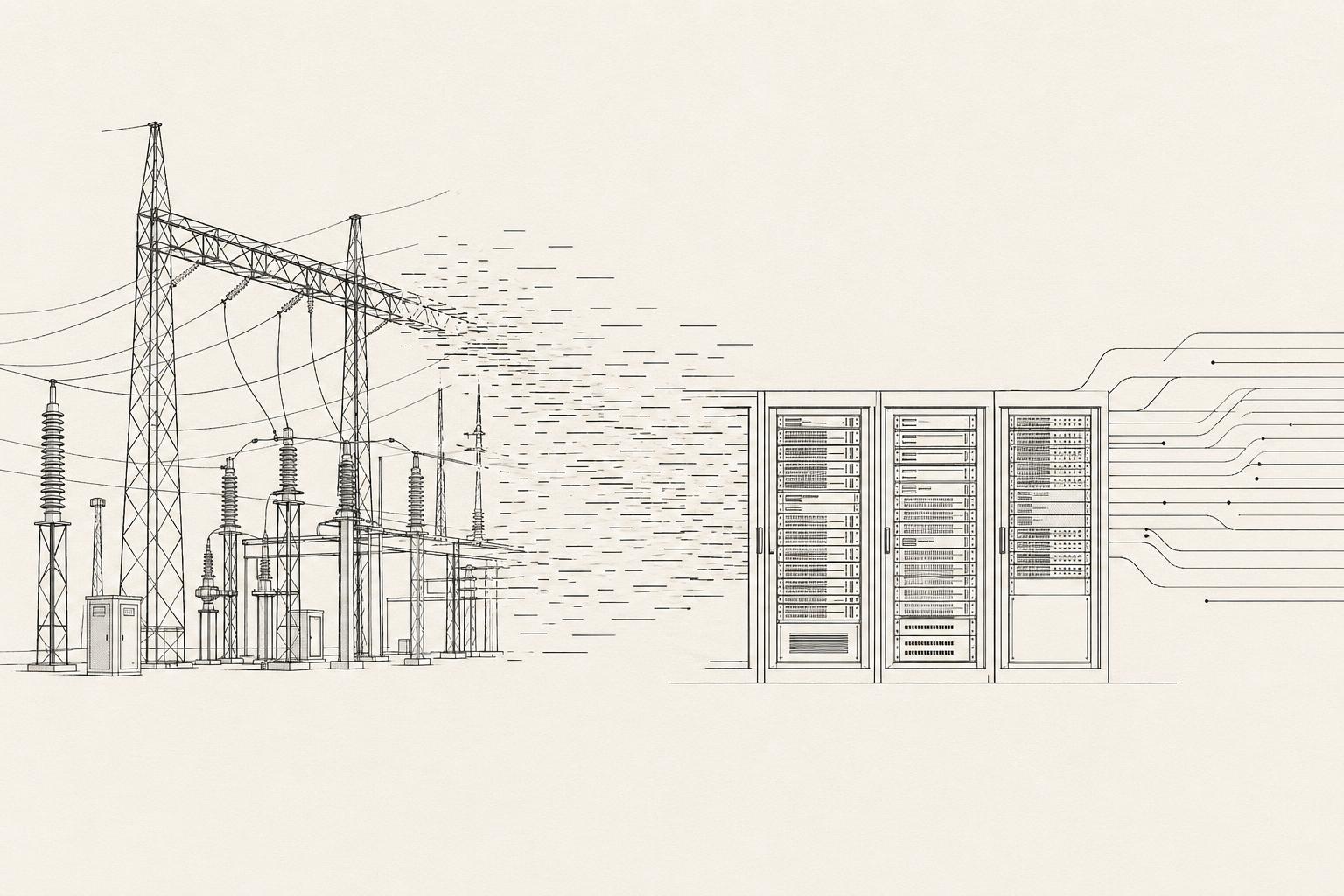

The trouble is that artificial intelligence is not mainly a language problem. It is not even mainly a software problem. At scale, it is an infrastructure problem. It is electricity, power quality, cooling, transformers, substations, land, permits, fibre, and long procurement chains dressed in prettier language.

The European Commission’s own AI material says this quite plainly if one bothers to read past the fanfare. The EU now counts 19 AI Factories and 13 AI Factory Antennas; at least 9 new AI-optimised supercomputers are to be procured, which the Commission says will more than triple current EuroHPC AI computing capacity. On top of that, the InvestAI facility is meant to mobilise €20 billion for up to 5 AI Gigafactories.[1]

But the revealing line is not the money. It is the quiet admission of what those gigafactories actually require: over 100,000 advanced AI processors, yes, but also “power capacity, reliable supply chains, advanced networking, energy efficiency”.[1] There it is. The entire matter in one bureaucratic sentence.

Europe Mistakes Governance for Capacity

Europe has become very good at mistaking governance for capacity. We regulate industries we do not dominate. We produce elegant standards for systems we no longer fully build. We confuse the ability to describe the future with the ability to provision it.

This is not only an AI problem. It is now a continental habit. The same reflex appears in defence, energy, housing, heavy industry, and culture: a preference for frameworks over force, administration over throughput, curation over production.

In AI, that reflex is especially dangerous because the underlying stack is so brutally physical. GPUs do not care how refined your white paper is. A cluster does not come online because a minister said the word ecosystem three times before lunch. Compute follows power. Then it follows everything power drags behind it: cabling, substations, cooling, maintenance crews, financing, grid access, political permission.

That is why I am suspicious of any European AI strategy that begins with talent narratives and ends with semicolons about values while treating energy as a side issue. It is not a side issue. It is the floor.

Expensive Power Is Not a Small Detail

Mario Draghi’s report on European competitiveness states the matter more bluntly than most politicians dare. Even after the crisis peak, EU companies still face electricity prices 2 to 3 times higher than those in the United States, while natural gas prices are 4 to 5 times higher.[2] That is not a decorative disadvantage. That is a tax on ambition.

Draghi also warns that lack of generation and grid capacity could limit Europe’s ability to make production more digital.[2] Again: the point is larger than chatbots. A continent with expensive power and constrained grids will struggle not only to train frontier models, but to diffuse AI throughout manufacturing, logistics, design, science, and public services. It will consume presentations about digitalisation more easily than the thing itself.

Eurostat’s latest electricity price data shows how awkward the landscape already is. In the first half of 2025, electricity prices for non-household consumers in the EU rose by 0.9% versus the same period a year earlier. They were highest in Ireland at €0.2726 per kWh and lowest in Finland at €0.0804 per kWh.[3] That is an enormous spread for a continent that enjoys talking about its single market as if it were a naturally coherent machine.

One should be careful here. Cheap electricity alone does not make a serious AI ecosystem. But persistently expensive electricity, uneven grid access, and slow capacity expansion make serious scale much harder. They encourage delay, dependence, and the sort of strategic delusion in which a place imagines itself to be leading because it is very busy hosting the conference.

AI Is an Industrial Load

The useful correction is simple: stop picturing AI as a cloud made of intelligence dust. Picture it as an industrial load.

Once you do that, much nonsense falls away. You stop asking only how to stimulate startups and start asking where the power will come from. You stop talking about digital leadership as a branding problem and start talking about network reinforcement, cooling water, power purchase agreements, land use, and equipment bottlenecks. You stop fantasising about frictionless scale and begin the dull adult work of physical provision.

This is also where Europe’s self-image becomes embarrassing. We still speak as if the noble part of technological leadership lies in drafting norms, while the crude part lies in building the ugly machinery. That is aristocratic nonsense. Every civilization that wants high technology must eventually learn to love transformers, switchgear, and maintenance. Otherwise it becomes a customer with opinions.

Asia has generally understood this more soberly. The serious states do not treat compute as a purely digital abstraction floating above the physical economy. They place it beside power, land, ports, fabs, industrial parks, and state capacity. One need not imitate every Asian method to learn from the discipline of the view.

The Real Risk

The real risk is not that Europe will have no AI activity. Of course it will. There will be labs, procurement rounds, pilots, consultants, accelerators, panels, model wrappers, and enough photo opportunities to kill a horse.

The risk is that Europe settles into the wrong layer of the stack: the compliance layer, the application layer, the orchestration layer, the tasteful layer. We will write the rules, rent the compute, import the chips, and congratulate ourselves on our ethical seriousness while the heavy capacity accumulates elsewhere.

That would fit an older European vice: preserving prestige after losing command of production. It is the museum instinct translated into digital policy. Beautiful values in the front room, somebody else’s machinery in the basement.

What Should Be Done

First, Europe should speak honestly. AI gigafactories are not merely innovation projects. They are power projects and industrial projects. Treat them accordingly.

Second, grid connection and power procurement for strategic compute infrastructure should be fast-tracked with the same seriousness Europe claims to reserve for industrial resilience. If a project can mobilise billions for processors but waits in a bureaucratic ditch for power, the strategy is unserious.

Third, energy affordability must be treated as digital policy. As long as European firms face structurally higher electricity costs than their US rivals, talk of continental AI leadership will remain scented rhetoric.

Fourth, public support for AI capacity should be tied to spillovers that actually matter: industrial deployment, applied research, workforce formation, heat reuse where sensible, and the strengthening of domestic technical ecosystems rather than mere symbolic occupancy.

Above all, Europe should stop flattering itself that seriousness lives in the abstract layer. Seriousness lives where the cable enters the ground.

The model begins at the substation. A continent that forgets this will not become sovereign in AI. It will become eloquent about dependency.

Sources

[1] European Commission, AI Factories (updated 23 April 2026):

19 AI Factories, 13 AI Factory Antennas, at least 9 new AI-optimised

supercomputers, more than tripling EuroHPC AI computing capacity;

InvestAI facility of €20 billion for up to 5 AI Gigafactories; each

gigafactory designed around more than 100,000 advanced AI processors and

requiring power capacity, reliable supply chains, advanced networking,

and energy efficiency.

https://digital-strategy.ec.europa.eu/en/policies/ai-factories

[2] European Commission / Mario Draghi, The future of European

competitiveness: A competitiveness strategy for Europe (Part A,

9 September 2024): EU companies still face electricity prices 2–3 times

those in the US and natural gas prices 4–5 times higher; lack of

generation and grid capacity could limit Europe’s digitalisation of

production.

https://commission.europa.eu/document/download/97e481fd-2dc3-412d-be4c-f152a8232961_en?filename=The%20future%20of%20European%20competitiveness%20_%20A%20competitiveness%20strategy%20for%20Europe.pdf

[3] Eurostat, Electricity price statistics (data extracted in

October 2025): non-household electricity prices in the EU rose by 0.9%

in the first half of 2025 compared with the same period in 2024; prices

were highest in Ireland (€0.2726/kWh) and lowest in Finland

(€0.0804/kWh).

https://ec.europa.eu/eurostat/statistics-explained/index.php?title=Electricity_price_statistics