Europe likes to speak as if sovereignty were a matter of communiqués. It is not. Sovereignty is tested in the vulgar places: the port, the transformer yard, the satellite layer, the cloud contract, the payment terminal.

Start with the terminal. Card payments are now the dominant electronic payment method in the EU, accounting for 70 billion payments and 54% of all non-cash transactions in 2023.[1] Yet in 2022, international card schemes accounted for roughly 61% of euro area card payments.[1] In the euro area, 13 countries rely on international card schemes entirely for all card transactions.[1] Only nine national card schemes remain active in the EU.[1]

That is the real picture. Europe has a sovereign currency in the abstract and a rented checkout in practice.

This is not a nationalist complaint about logos on plastic. It is a question of control over the most ordinary commercial gesture in the modern economy. Who sets the fee logic? Who shapes the product layer? Who owns the customer habit? Who decides what fails when systems are stressed? Who captures the data exhaust? Who enjoys the default position when commerce moves from cards to phones, subscriptions, wallets and invisible payments?

If the answer is mostly “not Europe”, then the sovereignty speeches require a little less fanfare and a little more shame.

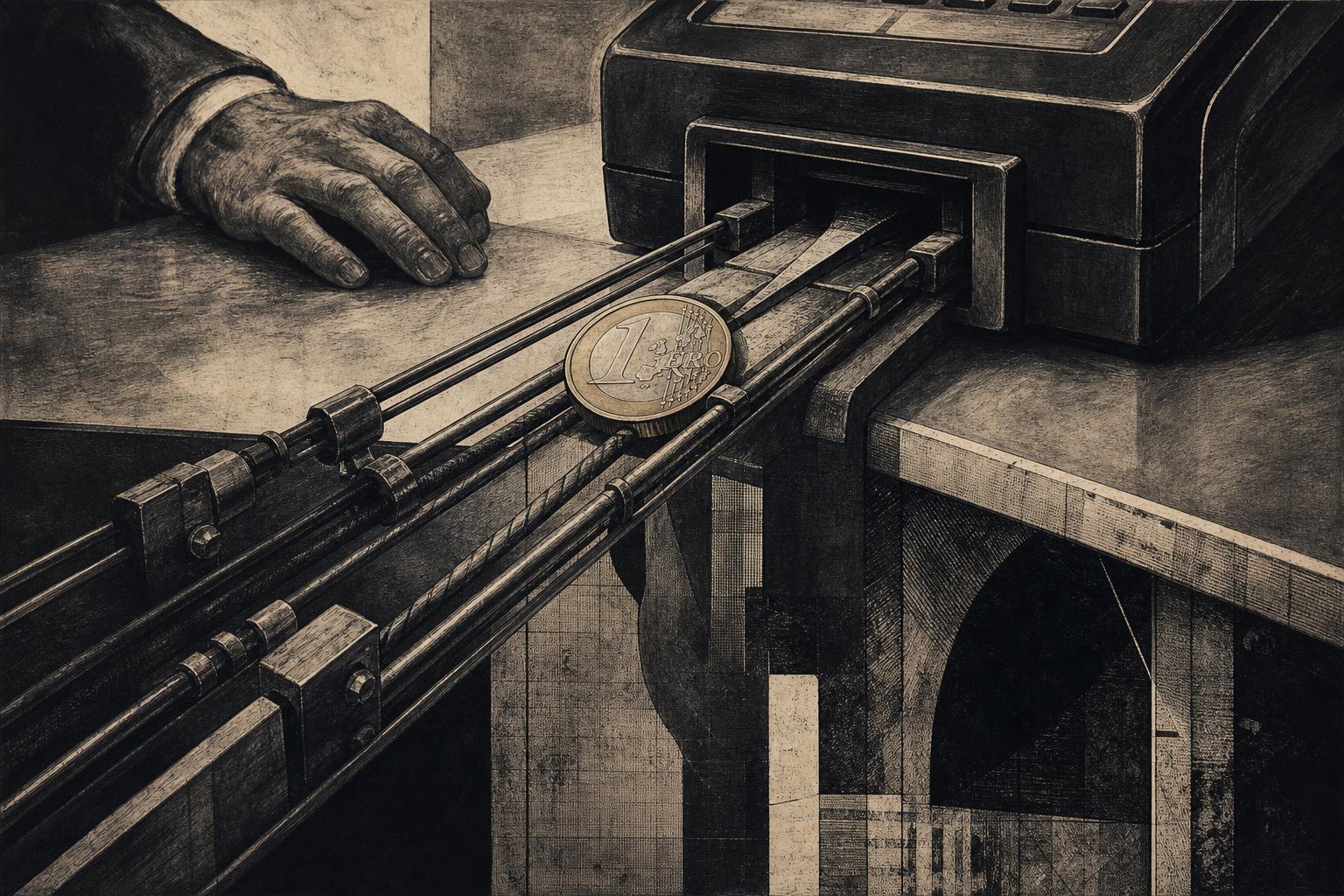

The Point of Interaction Is the Point of Power

The useful phrase in the ECB material is not glamorous. It is the point of interaction.[1] That is where payment becomes political economy: in the shop, online checkout, QR flow, recurring mandate, tap on glass, merchant terminal, bank app. The grand monetary architecture sits behind it, yes, but consumers and merchants live in front of it.

Europe has been stronger in the back room than at the counter. It can regulate fiercely, settle professionally, and issue solemn PDFs at industrial scale. It has been far less serious about owning the consumer-facing layer of payment. So the continent that gave itself a currency managed to outsource a remarkable portion of the gesture by which that currency moves through daily life.

This happened because dependency felt efficient. Foreign schemes were already there. They worked. Banks could save themselves the bother of building and defending something continental. Politicians could recite “single market” as if market integration and foreign dependence were interchangeable. For a while, the arrangement looked modern. So do casino carpets from a distance.

The cost appears later. Not only in fees, though fees matter. Not only in resilience, though resilience matters more than people admit. The deeper cost is strategic laziness. Once a society gives away the daily interface, it also gives away the habit of thinking that the interface matters.

Europe Built the Plumbing After Losing the Room

To be fair, Europe has not done nothing. It has done something extremely European: it built excellent plumbing.

The ECB’s instant-payments work is serious. Under the SEPA Instant Credit Transfer scheme, euro payments can be made available within ten seconds, with the service running 24 hours a day, 365 days a year.[2] The ECB says plainly that wider deployment would increase customer choice, foster innovation, improve safety, and strengthen strategic autonomy for European payments.[2] Quite right.

The trouble is that plumbing is not the same as habit. A settlement rail is not yet a mass-market ritual. Europe can build the clean back-end and still lose the front-end if the user experience, merchant acceptance, brand trust, and default placement remain elsewhere.

This is a familiar continental vice. We comfort ourselves with the thought that technical soundness will eventually compel market behaviour. Sometimes it does. Often it merely leaves us with admirable infrastructure hiding behind a foreign interface.

The instant-payments agenda is necessary. It is not sufficient. The problem is not only that Europe needs faster account-to-account rails. The problem is that it has taken too lightly the last three centimetres between a hand and a terminal.

The Digital Euro Is Also a Confession

The digital euro should be read partly as an innovation project and partly as a confession note.

The ECB now says openly that there is no European digital payment option covering the entire euro area, and that 13 of the 20 euro area countries are reliant on international card schemes for card payments.[3] Its proposed answer is a European electronic means of payment, free of charge for basic use and accepted across the euro area.[3]

Again: quite right. But notice what sort of sentence this is. A monetary union of nearly 350 million people, with a central bank capable of reordering bond markets, must explain that it still lacks a native digital payment option with full-area reach. That is not merely a product gap. It is a civilisational embarrassment.

The digital euro may prove valuable as a public utility, a fallback layer, a discipline device for the market, or a genuine retail option. I am not among those who dismiss it simply because the acronym gives off a faint scent of conference coffee. But even a good digital euro will not excuse the larger failure if Europe continues to neglect the commercial and merchant-facing layer above it.

A state that builds public money because it failed to cultivate robust private European payment reach is not wrong. It is merely arriving late, with paperwork.

What Seriousness Would Look Like

First, Europe should stop treating payments as fintech garnish. They are infrastructure. The payment layer is as real as an interconnector or warehouse network. It shapes bargaining power, resilience, data position and competitive life.

Second, instant account-to-account payment should become ordinary at the merchant level, not a noble side corridor for the already interested. Public services, large retailers, utilities, transport systems and digital commerce should all help normalise it. A pan-European rail that remains socially invisible is a museum piece with an API.

Third, regulators and banks should stop behaving as if voluntary coordination will eventually produce continental coherence by moral osmosis. It rarely does. If Europe wants a genuine payment option at scale, it must reward adoption, standardise acceptance and make the European route impossible to ignore.

Fourth, the consumer layer deserves as much discipline as the scheme layer. Design matters here. Reliability matters. Merchant integration matters. Trust matters. Asia understood this years ago: payment supremacy is won not only by clearing architecture but by making the act itself effortless, ubiquitous and faintly boring.

The Modest Conclusion Europe Dislikes

Europe does not lack intelligence, capital, regulatory force, or a currency. It lacks a certain kind of seriousness about ordinary systems. It enjoys the altitude of strategy and neglects the handrail.

That is why the payment question matters. It reveals a broader continental habit: preserving the language of power while outsourcing the mechanisms that make power routine.

Until Europe controls more of the checkout, its sovereignty talk will remain slightly comic. The euro may reign in treaties and central-bank vaults. In too much of daily life, it still arrives as a tenant.

Sources

[1] European Central Bank, Report on card schemes and processors and related press release, 28 February 2025: card payments were 70 billion transactions and 54% of all non-cash payments in the EU in 2023; international card schemes accounted for around 61% of euro area card payments in 2022; only nine national card schemes remain active in the EU; 13 euro area countries rely entirely on international card schemes; the report frames the issue in terms of strategic autonomy and the point of interaction.

https://www.ecb.europa.eu/press/pr/date/2025/html/ecb.pr250228_1~7f0697af45.en.html

https://www.ecb.europa.eu/pub/pdf/other/ecb.reportcardschemes202502~1614226b0a.en.pdf

[2] European Central Bank, What are instant payments?: instant payments make funds available within ten seconds; SCT Inst is available 24/7/365; the ECB states that wider harmonised instant-payments deployment would increase customer choice and foster innovation, safety and strategic autonomy for European payments.

https://www.ecb.europa.eu/paym/retail/instant_payments/html/index.en.html

[3] European Central Bank, Digital euro: there is currently no European digital payment option covering the entire euro area; 13 out of 20 euro area countries rely on international card schemes for card payments; the digital euro is presented as a European electronic means of payment accessible and accepted across the euro area and available free of charge for basic use.

https://www.ecb.europa.eu/euro/digital_euro/html/index.en.html